Initiating Coverage Of Apple (AAPL)

Is it time to take the bite?

Whilst the naysayer narrative is rising in volume, Apple fundamentals are improving and the stock chart looks bullish to my eyes.

I think the stock can move up nicely but, if wrong, there is a proximate and sensible stop level available.

Read on!

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Cestrian Capital Research, Inc., its employees, agents or affiliates, including the author of this note, or related persons, may have a position in any stocks, security, or financial instrument referenced in this note. Any opinions, analyses, or probabilities expressed in this note are those of the author as of the note's date of publication and are subject to change without notice. Companies referenced in this note or their employees or affiliates may be customers of Cestrian Capital Research, Inc. Cestrian Capital Research, Inc. values both its independence and transparency and does not believe that this presents a material potential conflict of interest or impacts the content of its research or publications.

Rumors Of Its Demise May Prove Exaggerated

by Alex King

Apple stock strength has defied weakening fundamentals for some time now. When markets dumped in H1 2022, the ex-growth no-innovation running-on-empty, Apple (AAPL) dropped by just 32% or so. When markets rebounded late in 2022, the same nothing-to-see-here $AAPL moved up quickly, gaining more than 50% in around six months to make a new all-time-high in July of 2023. So this thing has had both downside protection and upside potential.

To date we haven't covered the stock because I felt we had nothing different to say about it. Growth declining, product set atrophying? Sure. Yawn. Stock didn't care. Every analyst in town has something to say about AAPL, I personally found it all too boring to bother reading and decided that frankly I could get exposure to the upside by simply owning the Nasdaq, the S&P500 and/or the Dow Jones.

But now a lot of folks have a downer on the name. And that makes it interesting. Because at the same time that sentiment seems to have cooled some, the following things are happening.

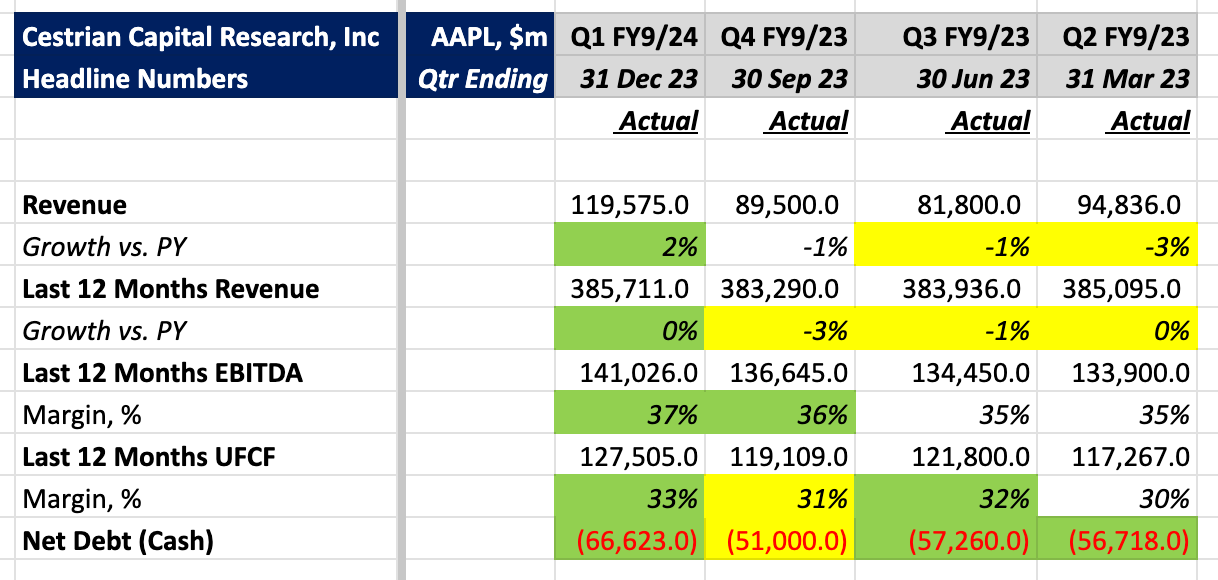

One, fundamentals are improving. You can read the detail below, but this simple table tells you most of the story.

Revenue is now growing on a quarter vs. PY quarter basis, and is up to flat on a TTM vs PY basis.

TTM EBITDA margins ticked up sequentially in the last two quarters, TTM cashflow in the most recent quarter.

The balance sheet is restocking with even more cash.

Innovation is returning to the company I believe. The car project was junked - a smart move I suspect in the face of tougher economics for EVs (lower demand, challenging resale values, increasing competition from Chinese and European vendors). This frees up a wall of money every year, and still more importantly frees up management time and emotion (bad projects kill management morale from midlevel supervisors up to and including the CEO), developer time and generally sets the company free to go do something more interesting instead.

One of three core product lines, Mac computers (remember them?), now utilizes fairly advanced silicon architecture - quasi-proprietary too. $ARM cores, lots of them, designed by Apple into fast, low power processors. If anything can nibble at Nvidia's market share in the near term, I suspect it is AAPL/ARM collaboration on GPU devices in AAPL hardware. And whilst one should never, ever, apply personal product experience to securities analysis, I find myself, a lifelong PC adherent now running a Mac-only business. Mac computers are hellishly expensive when shipped with the good silicon, but price/performance blows most everything out of the water. I don't know why any serious business user would buy anything else. This has nothing to do with the stock, but everything to do with a resurgence of innovation at the company which may, one day, deliver benefits for the stock.

VisionPro? I have no idea if it will take off or not, but it's the first new-category product Apple has come up with for some time, which one should applaud.

Services continues to grow; and the company has turned selling headphones into recurring revenue by designing a product that (1) everyone loses and has to re-buy and (2) even if you managed to not lose your tiny and physically unbalanced designed-to-tumble-out-of-your-ear itty-bitty buds then the battery will die soon enough, so you have to re-buy them. And nobody seems to mind. Genius.

Read on to get our Technical analysis (Wyckoff Zone limits, price target, stop levels), full set of fundamentals; valuation analysis, and stock rating. (The full text below is available to our paying Inner Circle and Tech Select Newsletter members.)

If you’ve yet to sign up as a paying member of Cestrian Tech Select Newsletter, you can do so by clicking on the button below.

For more information about Inner circle service and discount links, click below.