Is MongoDB A Compelling Stock To Buy Now?

The stock swooned after its Q2 earnings yesterday. We consider the risk-reward balance of buying this particular dip. Well, more of a trench than a dip.

DISCLAIMER: This note is intended for US recipients only and, in particular, is not directed at, nor intended to be relied upon by any UK recipients. Any information or analysis in this note is not an offer to sell or the solicitation of an offer to buy any securities. Nothing in this note is intended to be investment advice and nor should it be relied upon to make investment decisions. Cestrian Capital Research, Inc., its employees, agents or affiliates, including the author of this note, or related persons, may have a position in any stocks, security, or financial instrument referenced in this note. Any opinions, analyses, or probabilities expressed in this note are those of the author as of the note's date of publication and are subject to change without notice. Companies referenced in this note or their employees or affiliates may be customers of Cestrian Capital Research, Inc. Cestrian Capital Research, Inc. values both its independence and transparency and does not believe that this presents a material potential conflict of interest or impacts the content of its research or publications.

Fundamentals Weakened A Touch - Stock Dived Into the Accumulation Zone

If you're not familiar with MongoDB MDB 0.00%↑ this is a database software business which is gradually eating away at Oracle, IBM, and Microsoft's legacy database market share. The products are lightweight and fast in nature, initially deployed in high volume but low cost internet application setups, now found migrating towards more core enterprise functions.

Our friends at Software Stack Investing can help you dive deeper into the product - here.

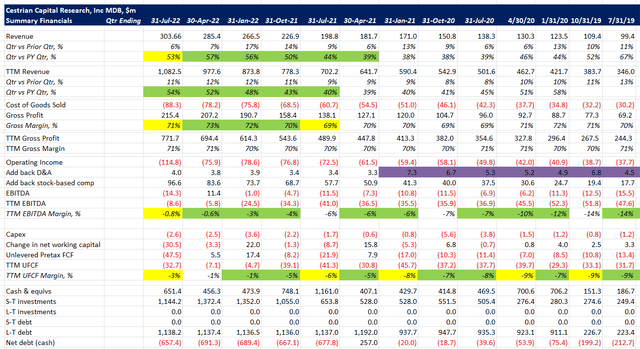

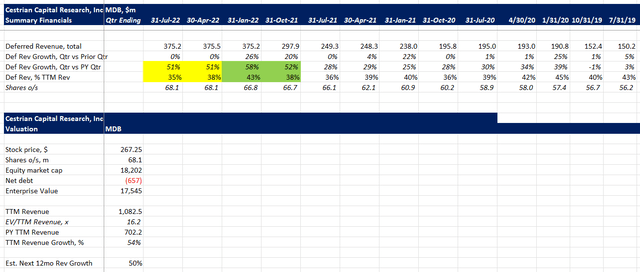

The company has historically operated on a payment-in-arrears business model which meant lower levels of deferred revenue vs. TTM recognized revenue than one might have hoped for. In recent quarters the company has sought to grow deferred revenue - meaning prepaid contracts - with gusto, and that has lent fundamental support to the rising stock price.

This quarter, deferred revenue growth was flat on the prior quarter - 51% up year on year in each quarter. This may be a harbinger of a coming decline, so whilst not a 'run for the hills' signal at this stage, it needs to be watched. For the last couple quarters we have seen this trend at a number of enterprise software companies. A natural reaction is to think, well, since there is economic doom and gloom everywhere, perhaps enterprise spending is slowing and this is where it is showing up first - in software purchases which don't absolutely have to happen in order to keep the lights on. And this may well prove to be the case. A notable exception was CrowdStrike CRWD 0.00%↑ which delivered very strong deferred revenue growth this quarter.

Here's the numbers.

Also disappointing this quarter was a reversal in the trend towards positive EBITDA and cashflow margins. Both took a step backward. This was driven it seems by a truly huge increase in spending in sales & marketing which if a response to what the management team believes is a wide open opportunity for the product set, should deliver improved revenue growth going forward (and with it most likely an increase in the revenue multiple at which the stock trades).

So we have recognized and deferred revenue showing a little weakness; a management team responding by cranking up the sales and marketing machine; we'll see if that works. Enterprise software sales cycles are long - nothing happens quickly. So assume the earliest you will see any benefit from the new spending is in say 6-12 months. (It could be as soon as 6 months because the ramp in sales spending started before this quarter).

Fundamentals are therefore OK - not great not terrible.

Let's turn to the stock chart, which gives us our zones in which we think the stock can be bought, sold, and where we think stop-losses can be placed. These actionable elements are for our paying subscribers only. If you’ve yet to become a paying member of this low-cost newsletter, you can sign up right at this link.